These days the financial crisis even affects Milan’s Fashion Week, which began last Thursday (2009-02-26) (see also Milan Fashion Week – 2008). IT Holding, the owner of Gianfranco Ferré and other famous labels was given bankruptcy protection, after racking up heavy losses and failing to find a buyer for its brands (see also Paris Fashion to organize Davos 2010).

It is obvious, the world is suffering a crisis of excessive indebtedness. To make matters more worrying, many governments, including the US, are too highly leveraged, as are many corporations such as banks. Moreover, US households are groaning under unprecedented debt burdens. So are there any lessons we may be able to learn from these economic woes? Read more below.

Lesson 1 – Protectionism and nationalism rule

Everybody agrees in public that protectionism and nationalism, while appealing to voters, will not help resolve the crisis. Nevertheless, French president Nicolas Sarkozy’s suggestion that Peugeot close its plants in Slovakia to save jobs in France tells another story.

As the tweets suggest, if debtors default, the main Austrian banks will be in serious trouble. While Austria can expect support if needed from Eurozone authorities before having to approach the International Monetary Fund (IMF), things are different for EU member states outside the Eurozone such as Bulgaria, Romania and Latvia. Will this result in an interlude of nationalization, followed by reorganization of new, narrowly focused retail banks in these countries? Nobody knows for now.

“It is justifiable if a factory of Renault is built in India so that Renault cars may be sold to the Indians. But it is not justifiable if a factory … is built in the Czech Republic and its cars are sold in France” – Nicolas Sarkozy, president of France.

2009-03-08: Without global co-ordination, ‘stimulus’ and ‘protection’ are two names for the same thing. The controversial ‘Buy American’ section in the US stimulus bill requires that only US-made steel and concrete be used in infrastructure projects.

Lesson 2 – Even government-owned zombies are unpleasant

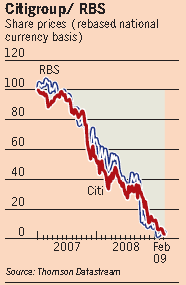

In a bid to avoid several bankruptcies among the bigger financial institutions, the UK and US governments have been swayed to take over a sizable share of private debt and provide billions worth of loan guarantees to RBS and Citigroup, respectively. But as the chart to the left shows, this did not stop those banks’ share prices from continuing to freefall.

In AIG’s case, the government took over 80 percent of the company, but this does little to avoid other tough choices. There is another $300 billion in net exposure that must be resolved. Obviously, even government-owned assets that are considered junk, are still trash and smell unpleasant. AIG’s insurance operations are buried by losses spewing from troubled parts of the business – $100 billion for 2008 alone.

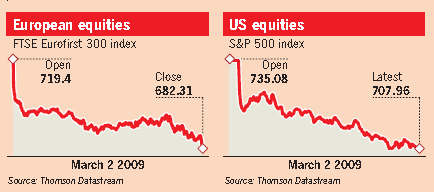

Investors understand this dilemma and this past Monday, stock markets dropped like rocks in conjunction with recent announcements made regarding dividend cuts (see charts below).

Banks lead the fall in share prices as Wall Street hits lowest levels since 1997.

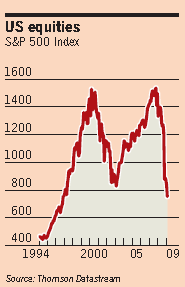

As the graphic to the right shows, US equities have been dropping for quite some time and this week does not give the impression that this trend may be changing anytime soon, whether for better or worse.

Lesson 3 – Capitalism for profits, socialism for losses

Besides that, even if government takes over stock or extends massive loans as described above, having all profits be distributed to managers while losses are absorbed by taxpayers is not only a potentially bad strategy, but no strategy at all.

Instead, managers must be offered the carrot and the stick. For example, failure to perform could be made to have consequences through deferred payment schemes or ‘claw-backs’.

It cannot be that neither Vikram Pandit (CEO of Citigroup) nor Oswald J. Grübel (new CEO of UBS) nor Peter Forstmoser (Chairman of the Board of Directors Swiss Re) do not partake in further losses, while reaping the rewards from future profits.

Lesson 4 – Paying cash for trash

The above illustrates that neither governments taking over bad debt nor losses is a good move for taxpayers. Unfortunately, it also does not make sense to invest in ventures whose futures are bleak, to say the least.

Opel cannot survive on its own; producing 1.5 million cars is considered too low a number to survive in its market segment. But Germany carrying all the risk for GM (i.e. giving the cash it needs to survive while GM provides little, if anything), is not the solution.

Still, Germany is not alone: Canada has been asked to invest CDN$900,000 for each job that might be saved by GM.

So will European governments be strong and smart enough to resist the car-maker’s urgent appeal for state aid so they can avoid closing three out of 10 factories to get rid of overcapacity in Europe? What is really needed to avoid closing plants and save jobs at GM in both Europe and Canada, is further voluntary redundancies, pay cuts and implementing part-time work. Even then, the survival of the Opel and Vauxhall brands as well as Canadian plants in their current form seems unlikely.

So why throw good money after bad? Is it to pacify the public? Certainly, it is not to save money, considering how much will have to be spent for each job to be saved.

=========>

Here’s my suggestion for today. What is your take, how do you perceive this situation as a shareholder or taxpayer?

Please share your insights and write a comment below. Thanks and I look forward hearing from you.

=========>

More resources:

Financial crisis – what shall we do?

Pingback: World Economic Forum

Pingback: World Economic Forum

Pingback: Citigroup, RBS and Google: Loads in common